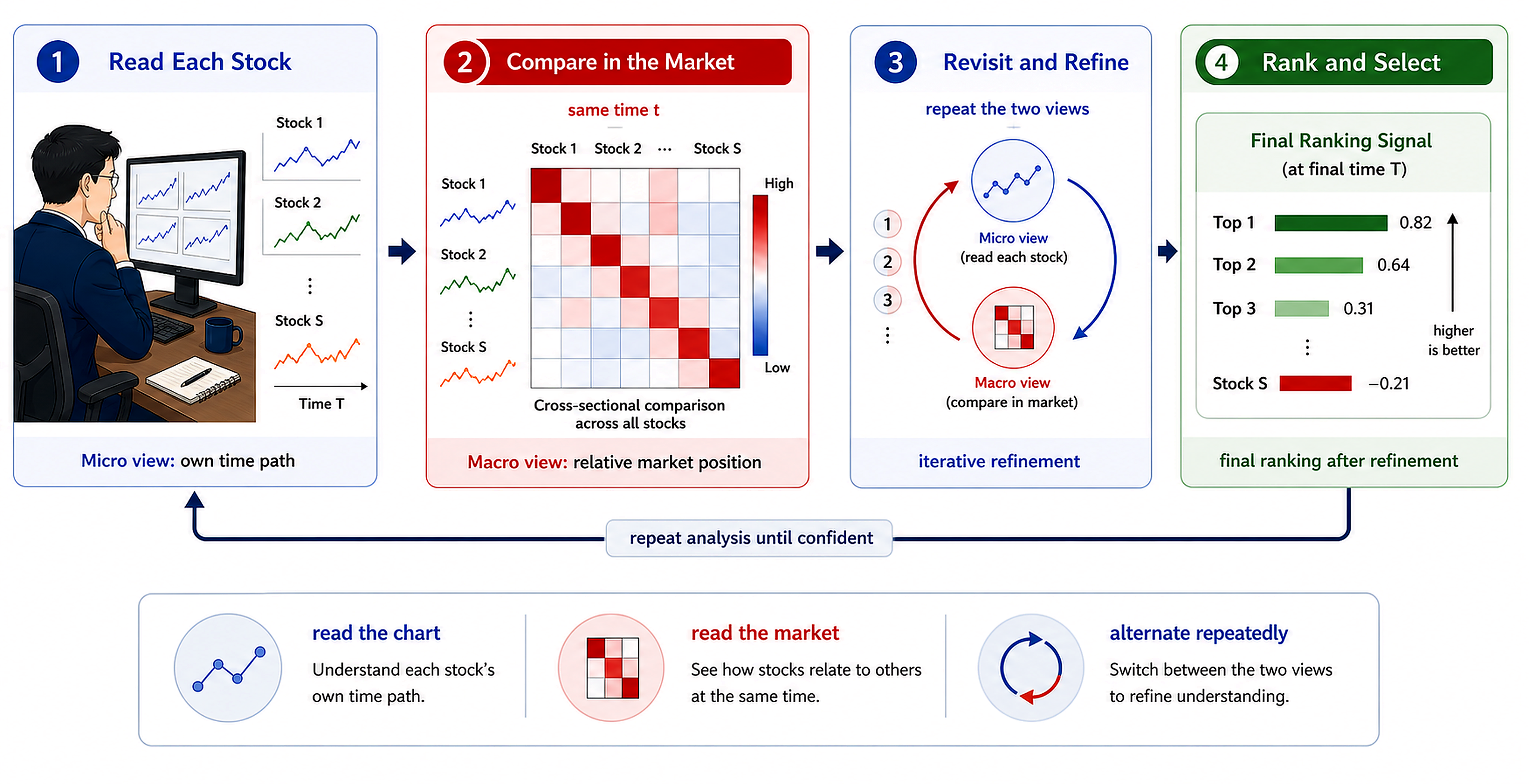

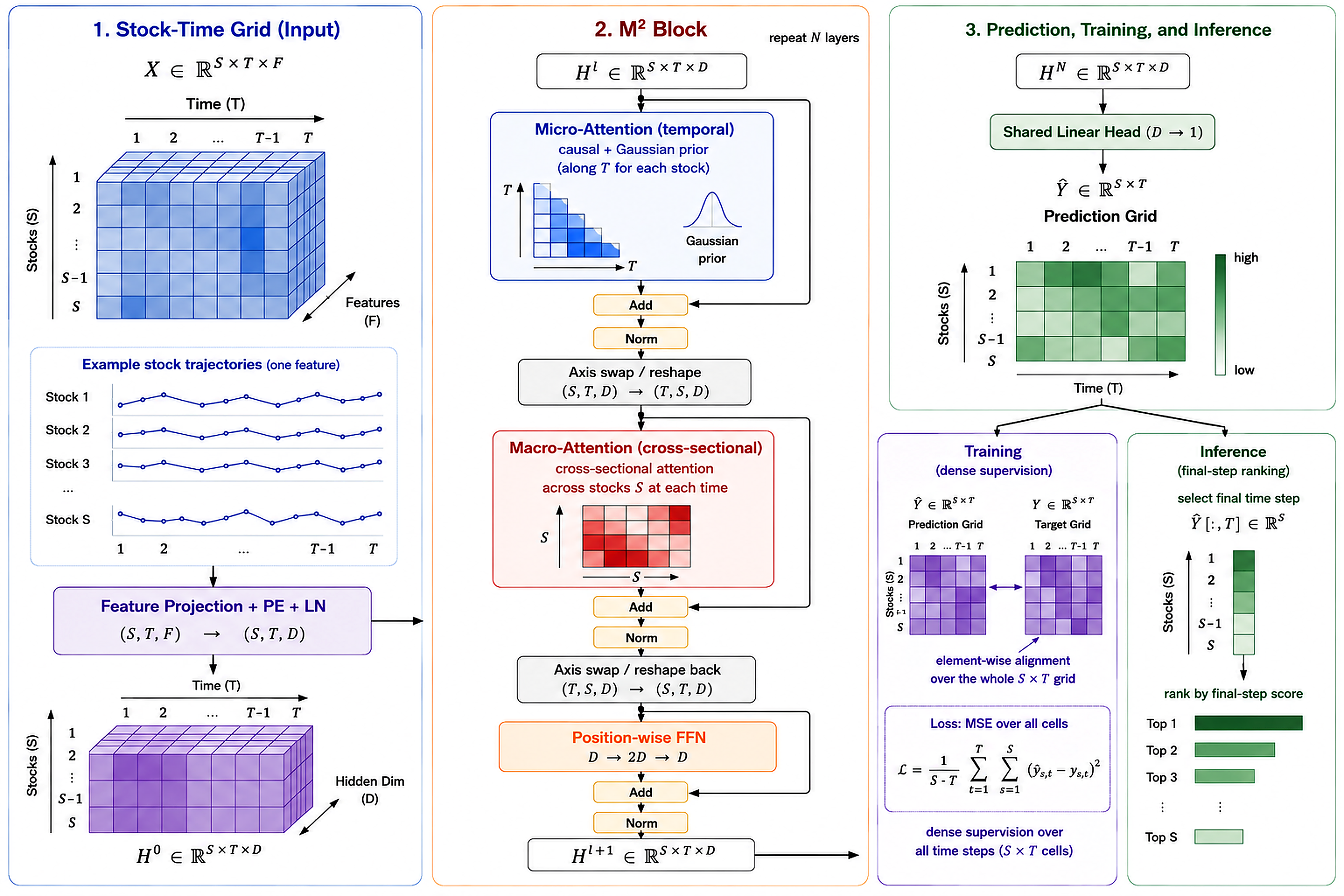

The architecture diagrams and M² Block notes show how the model reads single-stock time paths and same-day cross-sectional relations together.

Entry · — · Buy at Open

M-0-M cross-sectional Top 7 picks · Based on the — close · Rebalance at 09:30 on the next trading day

| # | Code | Name | Industry | Score | Signal | Ref Price | Weight |

|---|

📋

Strategy: the public baseline is M-0-M; M-1-M / M-2-M historical capability curves are shown on the Backtest page.

Rules →

Daily Review · — samples

The M-0-M public baseline uses the unified benchmark engine with its selected Top 7, sell-rank 35, and max-three-per-industry strategy, plus the same signal lag, open NAV, and fee accounting.

Avg Daily Excess

+0.00%

Top 7 average return minus CSI 300

Daily Win Rate

0.00%

— / — days Top 7 beat the benchmark

Stock Hit Rate

0.00%

Share of holdings beating the benchmark

Best Day

+0.00%

—

Last 60 days · Top 7 portfolio vs CSI 300 Beat Trail

Last 10 days · Holdings and realized performance

— / —

OOS Backtest · 1M Initial Capital · NAV Curve

M-0-M is the stable public baseline for this page. M-1-M and M-2-M are virtual historical research lines built on a local full-factor panel, shown only to compare model capability under one benchmark protocol. M-1-M / M-2-M stop on 2026-06-10; they are not new daily picks.

LATEST

M-2-M latest capability line

Frozen backtest on the full-factor panel: cumulative —, Sharpe —, MaxDD —.

→

Final NAV

1M initial capital → period end

Cumulative

+0.00%

CSI 300 over the same period —

Excess Return

+0.00pp

After fees

Monthly Win Rate

0%

—

Max Drawdown

0.00%

Maximum drawdown in range

Sharpe Annualized

0.00

Return / volatility · annualized

NAV Curve · M-0-M / M-1-M / M-2-M vs CSI 300 M-0-M M-1-M M-2-M CSI 300 Drawdown

Monthly Returns · Model vs CSI 300 Monthly excess win rate — / —

Model Preference · Based on all Top 7 holdings in range

Top 7 Industry Distribution

12 Most Frequent Holdings

RESEARCH-TO-REPRODUCTION REPOSITORY

What M²-Alpha Is

M²-Alpha (Micro-Macro Alpha Engine) is a deep-learning alpha repository for A-share cross-sectional stock selection. It packages model design, training logic, released weights, benchmark rules, and this public dashboard into one readable, reproducible, research-friendly project.

M-0-M, M-1-M, and M-2-M correspond to the trading-day refreshed compact release baseline, the canonical 3-block line, and the deeper 5-block iterative line. Full method details, training entry points, factor contracts, and backtest scripts are maintained in the GitHub repository and the technical report.

Released weights3

Input factors35

Backtest engineUnified

LicenseApache 2.0

Use the model zoo to separate the compact 3-block family from the deeper iterative 5-block line.

The factor page lists all 35 inputs, their intended role, and which fields are missing or approximated in public/open-data sources.

Run the benchmark with a compatible full panel; with only free public data, treat the output as an open-data baseline.

ARCHITECTURE

Micro-Macro Alpha Architecture

M²-Alpha represents each trading-day universe as a three-dimensional stocks S × time T × factors F grid. Instead of collapsing every stock into one terminal vector too early, it preserves an S × T × D representation across the whole window, so temporal Micro attention and cross-sectional Macro attention can repeatedly reread the panel inside stackable M² Blocks.

S × T × F, where S is stock count, T=8 is lookback length, and F=35 is the daily factor set.D=128, combined with positional encoding and normalization, producing H0 ∈ R^(S×T×D).S × T prediction grid; inference uses only the final time step Y[:,T] for daily cross-sectional ranking.This design lets path interpretation and relative-strength comparison correct each other. A deeper model is not just more parameters; it allows Micro and Macro to exchange context over more refinement rounds.

TECHNICAL REPORT

Full PDF technical report The report contains method diagrams, experiment settings, ablations, and reproduction boundaries. The PDF and repository docs are the source of truth.MODEL ZOO

Three Model Designs

The three released weights share the same stock-time grid → M² Block → dense prediction grid route. Lookback length, hidden width, Micro/Macro attention heads, and the Gaussian neighbor prior stay aligned. The main differences are release positioning, the canonical 3-block checkpoint, and the deeper 5-block iterative variant.

Shared base T=8 · F=35 · D=128

Micro heads 4

Macro heads 2

Gaussian σ=4

Dense supervision

M-0-M

compact release anchor · 3 blocksCompact release baseline. It is the smallest readable, runnable, maintainable M² stack: three M² Blocks, Micro reading each stock path first, Macro then reordering same-day stock relationships, with no extra gating complexity. It anchors the repository with a stable implementation.

- Prioritizes stability and transparency as a release/reference line.

- Belongs to the same 3-block family as M-1-M, not a separate architecture.

- Refreshes only after a validated A-share session with fresh data; weekends and holidays keep the last valid result.

3 blocksrelease anchorno extra gating

M-1-M

canonical 3-block lineFirst-generation canonical line. It keeps 3-block depth and asks whether the base M² Block is already strong enough: dense supervision trains the whole prediction grid, while inference ranks only the final time step. This is the standard compact M²-Alpha form.

- Tests the first-order value of decoupled Micro/Macro modeling plus iteration.

- Structurally close to M-0-M; the distinction is mainly checkpoint lineage and research protocol.

3 blockscanonical M²dense grid

M-2-M

deep iterative line · 5 blocksSecond-generation deeper line. It stacks M² Blocks to five layers, giving Micro more chances to reread time paths and Macro more rounds to correct relative positions. Depth here means cross-sectional context injected by Macro flows back into the next Micro pass, then gets recalibrated again.

- Targets stronger representation of co-movement, industry crowding, and relative strength.

- The only version that materially changes block depth and iteration count.

5 blocksmore refinementcapacity line

Along the design axis, M-0-M and M-1-M are compact same-depth lines, while M-2-M is the deeper iterative line. Factor completeness and public-data limits are documented separately in Data & Factors and Quick Start.

DATA AND FACTORS

35 Input Factors

M²-Alpha uses 35 input factors covering momentum, moving-average deviation, volatility, candlestick shape, trading activity, turnover, valuation, and money-flow structure. Each factor is first constructed along each stock history, then robust z-scored cross-sectionally on the same trading day before entering the M² Blocks. The closer the factor panel is to the full contract, the closer the model gets to its research-training and strong-backtest capability.

Momentum Returns

8 factors- What

- Cumulative returns over multiple past windows.

- Role

- Helps the model identify short-term continuation, reversal, and medium-term trend strength.

- Formula

close / close.shift(k) - 1, withk=1,2,3,5,10,20,30,60.

f_ret_1 · f_ret_2 · f_ret_3 · f_ret_5 · f_ret_10 · f_ret_20 · f_ret_30 · f_ret_60

Moving-Average Deviation

5 factors- What

- Close price relative to moving averages at different horizons.

- Role

- Provides a reference for overheated, weak, or equilibrium-breaking price behavior.

- Formula

close / rolling_mean(close,k) - 1, withk=5,10,20,30,60.

f_close_ma_5 · f_close_ma_10 · f_close_ma_20 · f_close_ma_30 · f_close_ma_60

Return Volatility

5 factors- What

- Rolling standard deviation of recent daily returns.

- Role

- Captures risk, disagreement, and instability, helping separate strong trends from noisy swings.

- Formula

- Compute 1-day return first, then

rolling_std(ret_1,k)withk=5,10,20,30,60.

f_vol_5 · f_vol_10 · f_vol_20 · f_vol_30 · f_vol_60

Candlestick Shape

4 factors- What

- Normalized body, full range, upper shadow, and lower shadow for the day.

- Role

- Captures intraday buying/selling pressure, failed breakouts, rebounds, and range structure.

- Formula

- Normalize by

open:(close-open)/open,(high-low)/open, and shadow ratios.

f_kmid · f_klen · f_kup · f_klow

Trading Activity

5 factors- What

- Volume relative to its own rolling mean, plus one-day changes in volume and amount.

- Role

- Detects volume expansion/contraction, shifts in trading heat, and participation behind price moves.

- Formula

vol / rolling_mean(vol,k)withk=5,10,20; alsopct_change(vol,1)andpct_change(amount,1).

f_vol_ratio_5 · f_vol_ratio_10 · f_vol_ratio_20 · f_vol_chg_1 · f_amount_chg_1

Turnover & Volume Ratio

3 factors- What

- Share turnover speed, free-float turnover, and the vendor-style volume ratio.

- Role

- Measures crowding, short-term attention, and abnormal trading activity.

- Formula

- Use

turnover_rate,turnover_rate_f, and vendor-stylevolume_ratio, then cross-sectionally standardize.

f_turnover_rate · f_turnover_rate_f · f_volume_ratio

Valuation Position

3 factors- What

- TTM P/E, P/B, and TTM P/S.

- Role

- Adds valuation context to price-volume signals, helping distinguish trend, crowding, and fundamental pricing position.

- Formula

- Read

pe_ttm,pb, andps_ttm, handle outliers, then apply same-day robust z-score.

f_pe_ttm · f_pb · f_ps_ttm

Money-Flow Structure

2 factors- What

- Main-fund net inflow intensity and the directional gap between large and small orders.

- Role

- Adds order-flow behavior, helping tell whether price movement is driven by active buying, active selling, or scattered trades.

- Formula

net_mf_amount / amount; and(buy_lg + buy_elg - buy_sm) / (buy_lg + buy_elg + buy_sm + 1).

f_mf_net_ratio · f_mf_big_small_diff

f_volume_ratio, f_mf_net_ratio, and f_mf_big_small_diff cannot be obtained as stable full-history truth fields; f_turnover_rate_f may only be approximated. The model is closest to research capability when the full factor panel is available.

PORTFOLIO STRATEGIES

The Actual Selection and Rebalancing Rule

Equal-weight high-scoring stocks; replace only after a clear rank deterioration

After each market close, the model scores every stock in the candidate universe. Higher scores receive priority. The portfolio first keeps existing holdings that remain inside the sell threshold, then fills vacancies from the highest-scoring stocks subject to an industry limit. The final portfolio is equal-weighted and trades at the next session's open.

What happens on each trading day

Day D close

Review the existing 7 holdings

Keep a tradable holding while its model rank remains inside the Top 35; prepare to sell only after it falls to rank 36 or below.

Day D close

Fill the portfolio back to 7 names

Walk down from rank 1, skipping names already held, untradable names, and candidates that would put more than 3 holdings in one industry.

Day D+1 open

Rebalance to equal weights

Each target holding normally receives about 14.29%. Trades execute at the next open and each transaction is charged a 0.13% fee.

A simple example: suppose yesterday's 7 holdings rank

4 / 9 / 17 / 23 / 31 / 44 / 78 today. With sell35, the first five stay,

ranks 44 and 78 are sold, and two vacancies are filled from today's highest-scoring eligible names.

The strategy does not replace the entire portfolio with a fresh Top 7 every day. The sell35 threshold creates a buffer: a holding that slips from rank 7 to rank 8 is not sold; it is replaced only after the model view weakens beyond rank 35. The industry rule also does not select the “best three industries.” It normally prevents one industry from occupying more than three slots while stocks are added by score.

M-1-M and M-2-M use the same trading logic

The operation order is identical for all three models. Only the candidate universe, target size, sell threshold, and industry allowance differ. These values were selected on a declared historical window and then fixed for the published curves; they are not re-tuned every day.

| Model | Stocks scored each day | Hold | Sell an old holding when | Normally max per industry |

|---|---|---|---|---|

| M-0-M | CSI300 constituents | 7 equal-weight names | Its model rank falls outside Top 35 | 3 names |

| M-1-M | Top 1000 by latest month-end float market cap | 5 equal-weight names | Its model rank falls outside Top 200 | 1 name |

| M-2-M | Top 1000 by latest month-end float market cap | 5 equal-weight names | Its model rank falls outside Top 50 | 3 names |

An untradable existing position cannot be force-sold. If a strict industry limit makes it impossible to fill the target portfolio, the original research implementation relaxes that limit in the final fallback. M-0-M refreshes on validated trading days; M-1-M/M-2-M are frozen historical research backtests.

Both result families are historical simulations. M-0-M refreshes never rewrite the frozen research curves. Real trading still requires fresh assessment of liquidity, slippage, execution constraints, and compliance requirements.

AGENT QUICK START

Prompt for a coding agent

The prompt below can be handed directly to a coding agent to set up the local environment, inspect data, launch the dashboard, or run a benchmark. It explicitly separates public display data from the full research factor panel to avoid mixing open-data output with full-factor research results.

Launch the static docs/ page and verify that M-0-M/M-1-M/M-2-M curves and model docs open correctly.

Inspect docs/METHOD.md, m2alpha/, and model_registry.yml, then explain the M² Block and three released weights.

If only public data is available, run only the public baseline. If a full 35-factor top1000 panel exists, run the research benchmark.

Ask the agent to record commands, data paths, strategy parameters, and output files so open-data baseline results are not mixed with full-data research results.

You are my coding agent. Help me configure and use the M2-Alpha repository:

1. Clone and enter the repository: github.com/Johnny-xuan/M2-Alpha.

2. First read README.md, docs/METHOD.md, docs/DATA_SOURCES.md, docs/REPRODUCTION.md, and model_registry.yml.

3. Create a Python environment and install requirements.txt; do not modify model weights.

4. Launch the local site: python -m http.server 8765 --directory docs, then verify that the Backtest and About pages open correctly.

5. Explain the three model lines:

- M-0-M: compact release baseline, 3-block M² stack, suitable for checking the implementation and public display.

- M-1-M: first-generation canonical line, also 3-block, useful for understanding the standard base M² Block form.

- M-2-M: second-generation deeper line, 5-block, useful for understanding the extra representation capacity from deeper Micro/Macro iteration.

6. Important data boundary:

The public/open-data path does not include the full research data. Training and strong benchmark results used a richer research panel,

including the full 35 factors, dynamic top1000 stock universe, volume ratio, free-float turnover, valuation, and money-flow fields.

If I only provide free BaoStock/AKShare/efinance data, clearly state that it cannot fully reproduce the M-1-M/M-2-M research capability.

7. If I want to reproduce the benchmark, first ask me for a compatible panel path. Start with the fixed protocol:

n_hold=5, sell_rank=200, max one name per industry, open execution/open NAV, fee_rate=0.0013.

Then use scripts/sweep_strategy.py on fixed weights and predictions to verify the selected curves:

M-1-M Top5/sell200/max-1-industry and M-2-M Top5/sell50/max-3-industry.

8. Finish with a short report: what code was run, where the data came from, what outputs were produced, and which factors remain unreproducible.The public repository can open-source code, weights, and workflow, but it cannot bundle the full research data used for training. To reproduce the strong research curves, prepare a compatible full factor panel; with only free public data, treat results as an open-data baseline.

OPEN LICENSE

Open License and Commercial Use

The M2-Alpha repository is released under the Apache License 2.0. Code, model weights, training scripts, backtest code, and the web dashboard may be used for academic research, derivative development, and commercial projects, provided that the license and required copyright notices are preserved.

Data should be considered separately: BaoStock, AKShare, efinance, and any data source you connect yourself have their own terms and upstream restrictions. The repository provides construction and adapter logic, but it does not guarantee the authorization scope of external data.

RISK NOTICE

Risk Notice

- This is not investment advice in any form. The site displays model predictions and historical backtests.

- Past backtests do not imply future performance. Model effectiveness may decay as market structure changes.

- The historical backtest includes a worst single day of — on —; real trading must tolerate short-term drawdowns.

- Executing differently from the rules, such as buying only a few names, using unequal weights, or delaying rebalance, can materially change realized results.

- Real trading requires independent assessment of fees, slippage, capital size, risk tolerance, and compliance constraints.

- Any decision made based on this site is the user's own responsibility.